TDS on Purchase under Section 393 – Income Tax Act, 2025

TDS on Purchase under Section 393 – Income Tax Act, 2025

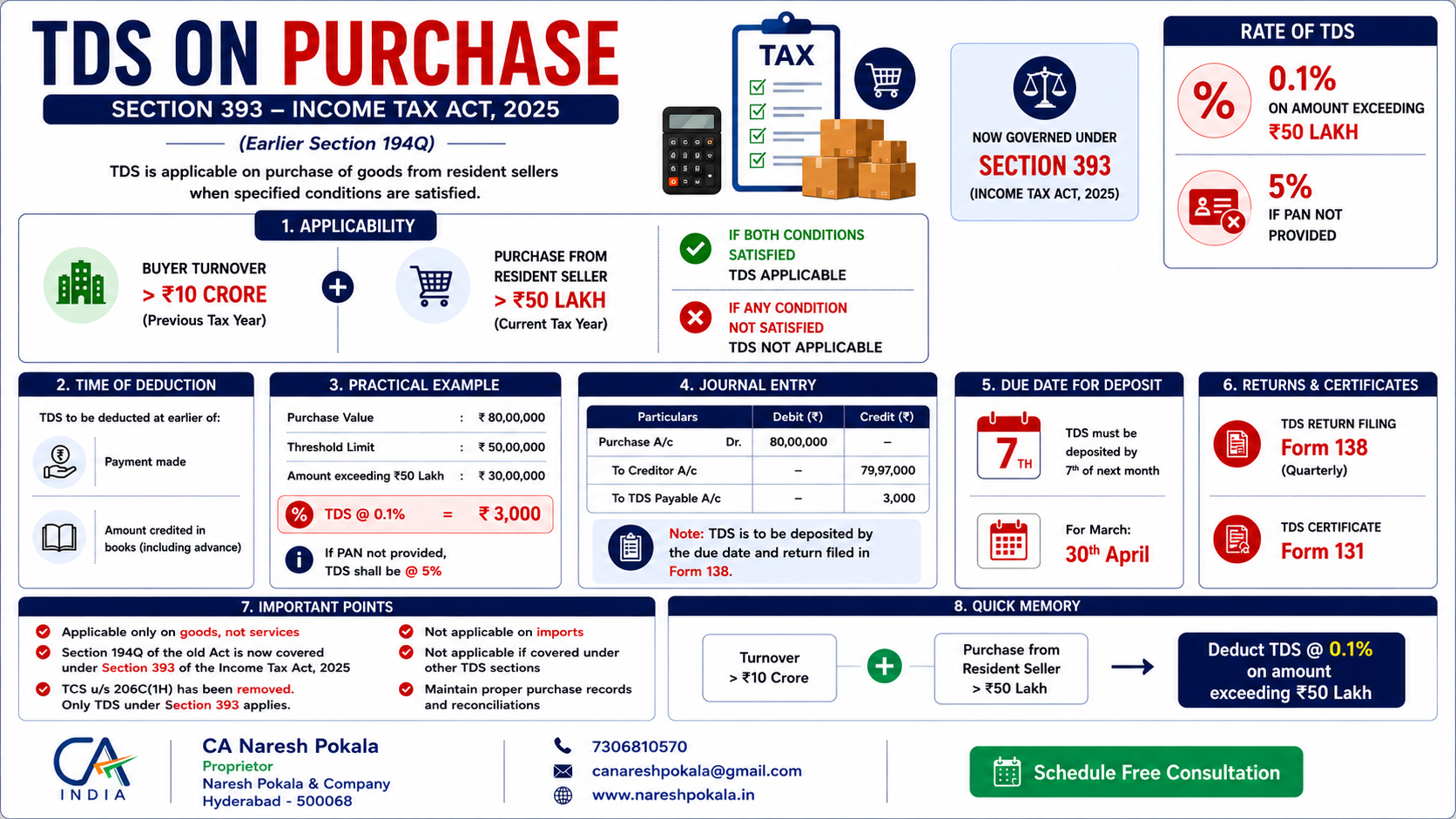

TDS on Purchase under Section 393 of the Income Tax Act, 2025 (earlier Section 194Q) applies to specified buyers purchasing goods from resident sellers. Businesses must comply with TDS deduction, deposit, and return filing requirements to avoid penalties and notices.

This article explains applicability, threshold limits, TDS rates, due dates, practical examples, and compliance requirements in simple language.

Applicability of Section 393

TDS under Section 393 becomes applicable when both conditions are satisfied:

Buyer Turnover Condition

- Buyer turnover exceeds ₹10 Crore in the previous financial year.

Purchase Threshold

- Purchase from a resident seller exceeds ₹50 Lakh during the current financial year.

If both conditions are satisfied, TDS provisions under Section 393 are applicable.

Rate of TDS

| Particulars | TDS Rate |

|---|---|

| Normal Rate | 0.1% |

| If PAN not provided | 5% |

TDS is applicable only on the amount exceeding ₹50 Lakh.

Time of Deduction

TDS must be deducted at the earlier of:

- Payment made to seller, or

- Amount credited in books (including advance)

Practical Example

| Particulars | Amount |

|---|---|

| Purchase Value | ₹80,00,000 |

| Threshold Limit | ₹50,00,000 |

| Amount liable for TDS | ₹30,00,000 |

| TDS @ 0.1% | ₹3,000 |

If PAN is not available, TDS will be deducted at 5%.

Journal Entry Example

Purchase A/c Dr ₹80,00,000

To Creditor A/c ₹79,97,000

To TDS Payable A/c ₹3,000

Due Date for Deposit

TDS deducted under Section 393 must be deposited by:

- 7th of the following month

- For March month: 30th April

Returns & Certificates

| Compliance | Form |

|---|---|

| TDS Return Filing | Form 138 |

| TDS Certificate | Form 131 |

Important Compliance Points

- Applicable only on purchase of goods.

- Not applicable on services.

- Applicable only for resident sellers.

- Not applicable on imports.

- TDS provisions apply only if not covered under other TDS sections.

- Maintain proper purchase records and reconciliations.

Quick Compliance Checklist

✅ Verify turnover eligibility

✅ Track vendor-wise purchases

✅ Deduct TDS at correct rate

✅ Deposit TDS before due date

✅ File quarterly TDS returns

✅ Issue TDS certificates timely

Conclusion

Section 393 aims to improve tax compliance on large purchase transactions. Businesses crossing turnover and purchase thresholds must monitor transactions carefully and ensure timely TDS deduction, deposit, and return filing.

Proper compliance helps businesses avoid penalties, notices, and interest liabilities under the Income Tax Act, 2025.

Have Questions? We're Here to Help

Get expert advice from NARESH POKALA & COMPANY. Reach out to discuss your requirements.