GST Notice Received? Here's Exactly What to Do First

Getting a GST notice can feel alarming — the moment you spot that official communication from the department, worry sets in almost immediately. But here is the reality: a GST notice does not mean you are in trouble. It means the department has a question, and you have the opportunity to answer it — correctly and on time.

In over a decade of helping businesses across Telangana manage GST compliance, I have seen thousands of notices. The vast majority are routine scrutiny alerts, minor reconciliation mismatches, or standard procedural requests. With the right approach, most close without any penalty or demand at all.

What makes the difference? Acting calmly, acting quickly, and acting correctly — in that order.

Why Does the GST Department Issue Notices?

Before we get into action steps, it helps to understand why notices are generated in the first place. The most common triggers include:

- Mismatch between outward supply data in GSTR-1 and tax declared in GSTR-3B

- Late filing or non-filing of GST returns

- Input Tax Credit (ITC) claimed against invoices the supplier has not filed

- Return scrutiny under Section 61 of the CGST Act

- Tax demand under Section 73 (genuine errors) or Section 74 (fraud/suppression)

- E-way bill discrepancies or incorrect invoice details

- Cancellation proceedings for taxpayers showing no activity

Identifying which of these applies to your notice is your very first task.

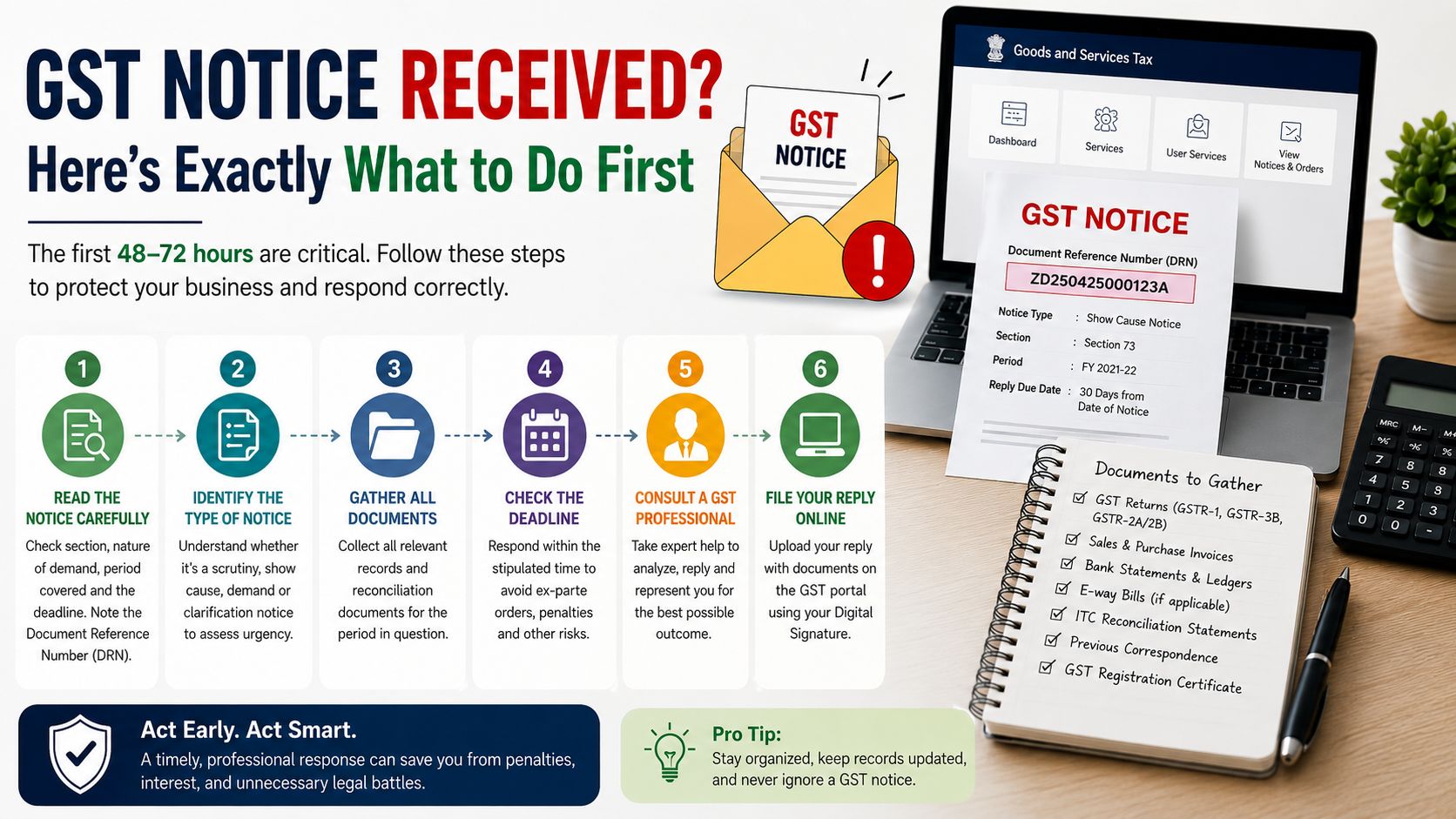

Step 1 — Read the Notice Carefully, in Full

This sounds obvious, but it is the step most taxpayers skip. They see "GST notice" and immediately forward it in a panic without reading it. Before doing anything else, read every line.

Note down the following:

- The notice number and date of issue

- The Form number (ASMT-10, DRC-01, GST REG-03, etc.) — this tells you the notice type

- The deadline to respond — typically 7, 15, or 30 days from issue date

- The tax period under question (which financial year or quarters)

- The nature of the discrepancy or query raised

- The amount of tax demand, if any stated

- The officer's name, designation, and contact

💡 Pro Tip: The deadline runs from the notice date, not the date you saw it. Log in to the GST portal under Services → User Services → View Notices & Orders and check the issue date immediately.

Step 2 — Identify the Type of Notice

The GST framework has over a dozen notice types. Each requires a different response strategy. Here are the most common:

| Form | Notice Type | What It Means |

|---|---|---|

| ASMT-10 | Scrutiny Notice | Discrepancy found between returns — common and often resolvable with documents |

| DRC-01 (Sec 73) | Demand Notice (Non-Fraud) | Tax appears short-paid due to genuine error — respond with reconciliation |

| DRC-01 (Sec 74) | Demand Notice (Fraud/Suppression) | Serious — requires urgent professional intervention |

| GST REG-03 | Registration Clarification | Inconsistency in registration application — reply within 7 working days |

| GST REG-17 | Show Cause for Cancellation | Department may cancel your GSTIN — file detailed reply immediately |

| GSTR-3A | Non-Filing Notice | Returns not filed — file pending returns at once |

| DRC-10 / DRC-13 | Recovery Notice | Demand confirmed, recovery proceeding — requires immediate CA/legal help |

Step 3 — Do Not Respond on Your Own

This is the single most costly mistake I see. A business owner, anxious to resolve things quickly, logs into the portal and types a hasty reply — sometimes inadvertently admitting to errors that do not exist, or providing incomplete documents that create more questions than they answer.

Your reply on the GST portal is a legal document. It can be used in any subsequent proceedings. A poorly worded response can concede ground in a case that could otherwise have been closed cleanly.

⚠️ DRC-01 notices that are not answered correctly can lead to confirmed demand orders (DRC-07) with 18% interest and penalties up to 100% of tax dues. Never respond to a DRC-01 without professional review.

Step 4 — Gather All Relevant Documents Immediately

While your CA prepares the response, start collecting documents. The faster you have them ready, the faster the matter moves.

For a scrutiny or mismatch notice (ASMT-10):

- GSTR-1 and GSTR-3B filings for the relevant periods

- Purchase invoices and GSTR-2A / 2B data

- Sales invoices for the disputed months

- Bank statements for the period under question

- E-way bill records if the discrepancy involves goods movement

For an ITC mismatch notice:

- All purchase invoices against which ITC was claimed

- GSTR-2A / 2B reconciliation worksheet

- Proof of receipt of goods or services

- Payment confirmation to the supplier (bank transfer records preferred)

- Evidence that the supplier has filed their GSTR-1 for the period

Step 5 — File the Reply Correctly and Well Before the Deadline

Once your advisor has prepared the response:

- Log in to gst.gov.in → Services → User Services → View Notices & Orders

- Locate the notice by its DRN (Document Reference Number)

- Click "Reply" and upload your response with all supporting attachments

- Submit using your Digital Signature Certificate (DSC) or EVC

- Save the ARN (Acknowledgement Reference Number) — this is your proof of timely response

Upload documents as clearly labelled PDFs, each under 5 MB. Do not upload bulk unlabelled files.

If you need more time, apply for an extension before the original deadline — you cannot request one after it has passed.

Step 6 — Follow Up and Track the Case

Filing the reply is not the end. After submission:

- Check the portal regularly for further orders or information requests

- Respond promptly to any additional queries from the officer

- Attend hearings if summoned — apply for adjournment in advance if needed

- If no order is received within 30 days of your reply, follow up through the portal or with the adjudicating officer directly

What Happens If You Ignore a GST Notice?

Ignoring a GST notice is never a safe choice. The consequences escalate automatically:

- Best judgement assessment — the officer determines your tax liability without your input

- Ex-parte demand order — confirmed without hearing your side; appeal is your only option

- Recovery proceedings — bank account attachment, property attachment

- ITC blockage under Rule 86A in fraud or serious mismatch cases

- Prosecution in cases involving deliberate evasion

A notice left unanswered is an open invitation for the worst possible outcome.

Real Client Story: When a Reporting Error Looked Like Tax Evasion

Industry: Electrical Goods Trading | Location: Hyderabad | Notice: GST ASMT-10 | Exposure: ₹1,80,000+

A trader dealing in electrical goods — a regular filer who had never missed a return — received a scrutiny notice in Form GST ASMT-10. The department's systems had flagged a gap between the outward supply figures in his GSTR-1 and the tax liability declared in his GSTR-3B across multiple quarters. On paper, the numbers did not match, and the inference was obvious: tax had been short-paid.

With potential interest and penalty exposure exceeding ₹1,80,000, the trader was understandably shaken. His first instinct was to draft a reply himself and submit it quickly. Fortunately, he came to us before doing so.

What we found: A transaction-level reconciliation of GSTR-1, GSTR-3B, books of account, and bank statements revealed the actual cause: certain invoices had been entered twice in the accounting software, causing them to appear twice in the GSTR-1 upload. The GSTR-3B was correct. There was no suppression, no evasion — just a duplicate entry that the software had silently compounded across several months.

What we did: We prepared a detailed invoice-level reconciliation identifying each duplicate entry with supporting evidence, drafted a legally sound reply letter presenting this clearly to the adjudicating officer, and filed the full submission through the GST portal well within the 30-day deadline.

The outcome: ✔ No additional tax demand was raised ✔ Penalty proceedings were not initiated ✔ The scrutiny case was formally closed ✔ The trader continued business without disruption or litigation

The lesson: A mismatch between GSTR-1 and GSTR-3B does not automatically mean tax has been evaded. The department's systems flag anomalies — they do not interpret them. A self-drafted reply that missed the duplicate-entry angle could easily have conceded a ₹1,80,000 liability that never actually existed.

Identifying details including name and specific figures have been changed to preserve client confidentiality. The nature of the issue and outcome are representative of this type of matter.

How to Prevent GST Notices Going Forward

Most GST notices arise from the same handful of recurring issues. Address these and your risk drops significantly:

- Reconcile GSTR-1 vs GSTR-3B every month before filing — any gap triggers scrutiny

- Reconcile GSTR-2B vs your purchase register before claiming ITC

- File all returns on time — late filings attract notices automatically

- Verify that your suppliers are filing — ITC is only safe when the supplier's GSTR-1 is filed

- Match e-way bill data with invoices — discrepancies in value, vehicle number, or distance are flagged

- Never split invoices to avoid e-way bill thresholds — this is detected easily

Quick Checklist: GST Notice Received

- Read the notice fully and note the DRN and deadline

- Identify the Form number and notice type

- Mark the response deadline in your calendar immediately

- Collect relevant returns, invoices, bank statements, and reconciliations

- Contact a qualified GST consultant — do not draft a reply alone

- File the reply through the GST portal before the deadline

- Save the ARN as proof of timely submission

About Naresh Pokala & Company

Since 2020, Naresh Pokala & Company, Chartered Accountants (Firm Reg. No. 022352S) has helped businesses across Hyderabad, Telangana and all of India handle GST notices, compliance, and disputes with confidence.

📧 canareshpokala@gmail.com | 📱 +91 73068 10570 | 🌐 ww.nareshpokala.in 📍 1st Floor, Janapriya Enclave, L. B. Nagar, Mansoorabad, Hyderabad – 500068

Free initial consultation available for GST notice matters.

Disclaimer: This article is for general informational purposes only and does not constitute legal or tax advice. Please consult a qualified GST practitioner for advice specific to your situation.

Have Questions? We're Here to Help

Get expert advice from NARESH POKALA & COMPANY. Reach out to discuss your requirements.