LLP vs Private Limited Company in India (2026): Complete Guide for Startups

LLP vs Private Limited Company in India (2026): Complete Guide for Startups

Choosing the right business structure is one of the most important decisions a founder makes. Get it right and your business is built on a solid legal and tax foundation. Get it wrong and you may face funding roadblocks, unexpected tax burdens, or compliance headaches down the road.

In India, the two most popular structures for serious businesses are the Limited Liability Partnership (LLP) and the Private Limited Company (Pvt Ltd). Both offer limited liability protection and a separate legal identity — but they differ significantly in taxation, compliance, fundraising ability, and operational flexibility.

This guide gives you a complete, accurate comparison for 2026 so you can make an informed decision before registering your business.

What is an LLP?

An LLP (Limited Liability Partnership) is a hybrid business structure introduced under the Limited Liability Partnership Act, 2008. It combines the flexibility of a traditional partnership with the limited liability protection of a company. Partners are not personally liable for the debts of the LLP beyond their agreed contribution.

LLPs are governed by the Ministry of Corporate Affairs (MCA) and registered with the Registrar of Companies (ROC).

What is a Private Limited Company?

A Private Limited Company is a separate legal entity incorporated under the Companies Act, 2013. It can have shareholders, issue equity shares, attract external investment, and offer Employee Stock Options (ESOPs) to employees. Directors manage the company on behalf of shareholders.

It is the most preferred structure for startups seeking growth, external funding, and long-term scalability.

LLP vs Private Limited Company — Complete Comparison 2026

1. Governing Law

LLP is governed by the Limited Liability Partnership Act, 2008. A Private Limited Company is governed by the Companies Act, 2013. Both are regulated by the Ministry of Corporate Affairs (MCA) and registered on the MCA portal.

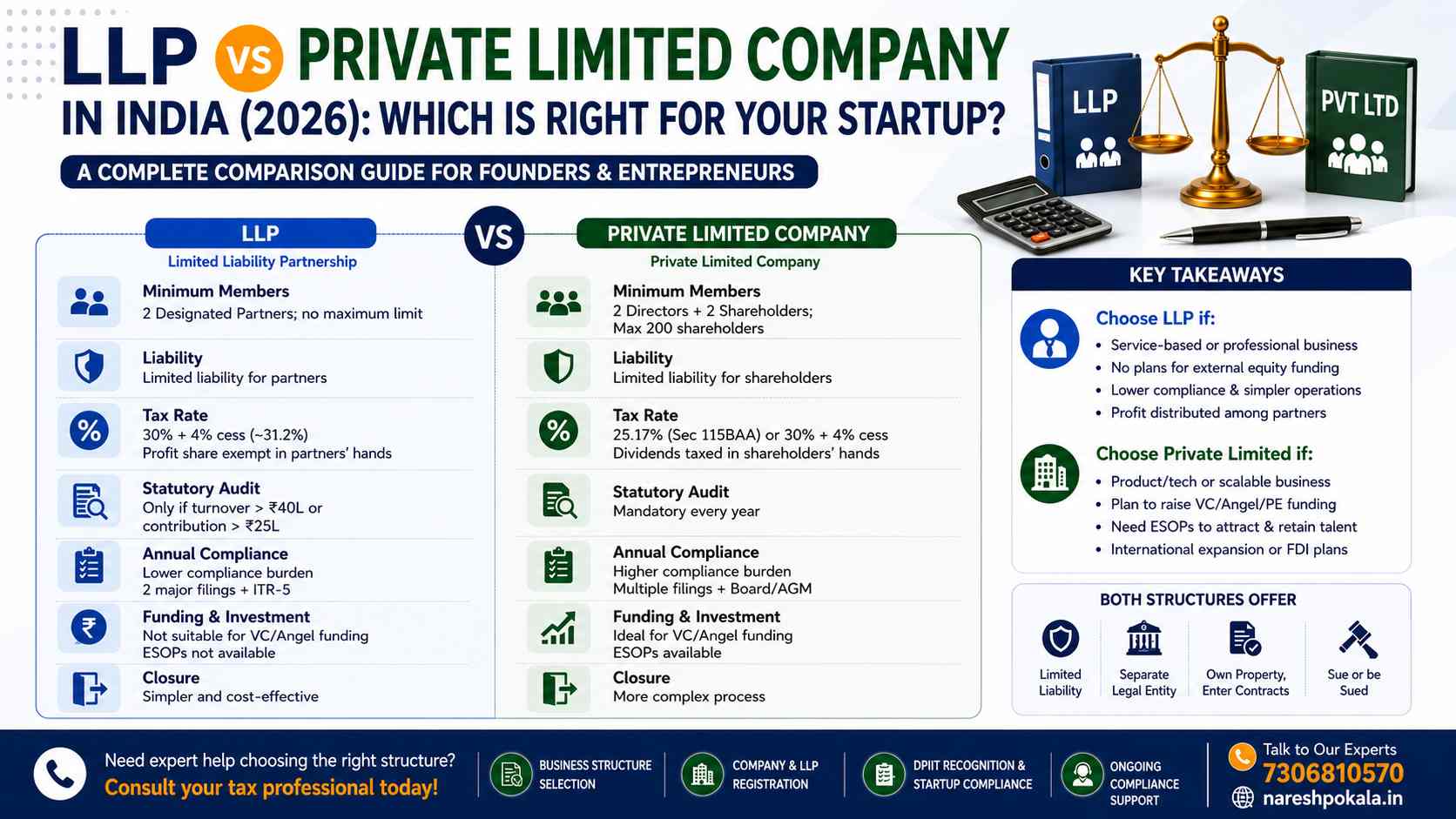

2. Minimum Members

An LLP requires a minimum of 2 Designated Partners with no upper limit on the number of partners. A Private Limited Company requires a minimum of 2 directors and 2 shareholders, with a maximum of 200 shareholders.

3. Limited Liability

Both structures offer limited liability protection. Partners in an LLP and shareholders in a Private Limited Company are not personally liable for the debts or obligations of the business beyond their agreed contribution or paid-up share capital. This is a critical advantage both structures share over sole proprietorships and general partnerships.

4. Separate Legal Entity

Both an LLP and a Private Limited Company are separate legal entities capable of owning property, entering into contracts, and suing or being sued in their own name — independent of their partners or shareholders.

5. Registration Process and Timeline

Both LLP and Private Limited Company registration typically take 10 to 15 working days on the MCA portal. The process for a Private Limited Company involves obtaining DSC (Digital Signature Certificate), DIN (Director Identification Number), name reservation through RUN, and filing SPICe+ form for incorporation.

LLP registration follows a similar process — DSC, DPIN, name reservation, and filing FiLLiP form — with one additional mandatory step: the LLP Agreement must be drafted and filed in Form 3 with the ROC within 30 days of incorporation. Many founders overlook this step and face penalties.

6. Taxation — The Most Critical Difference

This is where the two structures differ most significantly, and where the decision often comes down to your business model.

LLP Taxation:

- Flat income tax rate of 30% on total profits, regardless of income level

- 4% Health and Education Cess on tax payable

- Effective tax rate: approximately 31.2%

- Profit distributed to partners is fully exempt in their hands — there is no double taxation on profit distributions

- Partners can also receive remuneration (salary) and interest on capital from the LLP, subject to limits under Section 40(b) of the Income Tax Act — these are deductible as expenses in the LLP's hands and taxable as business income in the partners' hands, often resulting in lower overall tax outflow

Private Limited Company Taxation:

- Domestic companies with turnover up to ₹400 crore: 25% tax rate

- Domestic companies with turnover above ₹400 crore: 30% tax rate

- Under Section 115BAA of the Income Tax Act, 1961 (introduced in September 2019): any domestic company can opt for a concessional rate of 22%, with a flat 10% surcharge and 4% Health and Education Cess — resulting in an effective tax rate of 25.17%. Companies opting for Section 115BAA cannot claim most deductions and exemptions (such as Section 80-IA, 80-IAB, etc.)

- Under Section 115BAB: new manufacturing companies incorporated after 1st October 2019 and commencing production before 31st March 2024 can opt for 15% tax rate (effective ~17.16%)

- Dividends paid to shareholders are taxed again in the shareholders' hands at their applicable income tax slab rate — creating a two-level tax on the same profit

Key tax insight: At the entity level, a Private Limited Company under Section 115BAA (25.17% effective rate) pays less tax than an LLP (31.2%). However, when a company pays dividends to owners, that income is taxed again — making the combined effective tax rate higher than it appears. An LLP avoids this double taxation entirely. The right choice depends on whether you plan to reinvest profits (Pvt Ltd is better) or regularly withdraw them (LLP is more efficient).

7. Statutory Audit Requirements

This is one of the most practically important differences for small and growing businesses.

LLP: Statutory audit by a Chartered Accountant is required only if annual turnover exceeds ₹40 lakhs OR capital contribution exceeds ₹25 lakhs. LLPs below both thresholds can have their accounts self-certified by designated partners — no mandatory CA audit required.

Private Limited Company: Statutory audit by a Chartered Accountant is mandatory every year, regardless of turnover, profit, or size. Even a newly incorporated company with zero revenue must get its accounts audited.

8. Annual Compliance Requirements

LLP Annual Compliance:

- Form 11 (Annual Return): due by 30th May every year

- Form 8 (Statement of Accounts and Solvency): due by 30th October every year

- ITR-5 (Income Tax Return): 31st July for non-audit LLPs; 31st October for LLPs requiring audit

- DIR-3 KYC for each Designated Partner: 30th September annually

- Event-based filings for partner changes, address changes, or amendments to the LLP Agreement (within 30 days of change)

- Late filing penalty: ₹100 per day per form — with no maximum cap

Important: All annual filings are mandatory for every LLP, including those with no transactions or revenue during the year. There is no dormancy status under the LLP Act. An LLP that fails to file for two consecutive years risks being struck off the MCA register.

Private Limited Company Annual Compliance:

- Minimum 4 board meetings per financial year

- Annual General Meeting (AGM): on or before 30th September

- Form AOC-4 (Financial Statements): within 30 days of AGM

- Form MGT-7 (Annual Return): within 60 days of AGM

- Statutory audit: mandatory every year

- DIR-3 KYC for every DIN holder: 30th September

- Additional event-based filings for share allotments, director changes, charges, loans, and other corporate actions

- Late filing penalty: ₹100 per day per form — with no maximum cap

Verdict: LLP carries significantly lower compliance overhead and cost, especially for smaller businesses below the audit threshold.

9. Fundraising and Investment

This is the single most decisive factor for growth-oriented startups.

Private Limited Company: Can issue equity shares, preference shares, and convertible instruments to investors. This is the standard structure accepted by angel investors, venture capital funds, private equity, and foreign investors. It is the only structure through which a startup can raise equity funding in India.

LLP: Cannot issue equity shares or any equity instruments to investors. An LLP can only accept capital contributions from partners and loans from third parties. Venture capitalists and angel investors cannot become "shareholders" in an LLP — making it structurally incompatible with equity fundraising.

If you are building a startup with any plans to raise external funding — at seed stage, Series A, or beyond — a Private Limited Company is the only viable structure.

10. ESOPs (Employee Stock Options)

Private Limited Company: Can issue ESOPs to employees under the Companies Act, 2013. ESOPs are one of the most powerful tools for attracting and retaining senior talent at early-stage startups where cash compensation is limited.

LLP: ESOPs cannot be issued in the traditional sense, as there is no share capital. Partners can share profits, but there is no mechanism to offer equity-equivalent incentives to employees who are not partners.

11. FDI (Foreign Direct Investment)

Private Limited Company: FDI is permitted under the automatic route in most sectors — no prior government approval required. Widely preferred by foreign investors and multinational companies for India entry.

LLP: FDI is permitted under the automatic route only in sectors where 100% FDI is already allowed under the automatic route. Additionally, FDI in LLPs is subject to more restrictions — foreign investors cannot invest via convertible instruments, and profit repatriation requires compliance with FEMA regulations. This makes LLPs less practical for businesses with foreign investment.

12. Startup India (DPIIT Recognition)

Both LLPs and Private Limited Companies are eligible for recognition under the Startup India initiative and DPIIT (Department for Promotion of Industry and Internal Trade) certification.

Recognised startups — regardless of structure — can potentially avail:

- 3-year income tax holiday under Section 80-IAC of the Income Tax Act (subject to eligibility conditions)

- Exemption from angel tax under Section 56(2)(viib) of the Income Tax Act

- Self-certification for labour and environmental laws

- Fast-tracked patent and trademark applications

- Easier access to government tenders

Eligibility for Section 80-IAC and angel tax exemption is subject to specific conditions including date of incorporation, nature of business, and turnover limits. A Chartered Accountant should verify eligibility before applying.

13. Conversion: LLP to Private Limited Company

An LLP can be converted into a Private Limited Company under Section 366 of the Companies Act, 2013 read with the Companies (Authorised to Register) Rules, 2014.

The process involves:

- Obtaining consent from all designated partners

- Reserving the company name on the MCA portal

- Filing Form URC-1 along with required documents (LLP Agreement, certificate of registration, financial statements, partner details)

- Obtaining Certificate of Incorporation from the ROC

The LLP must have filed all pending statutory returns and have no outstanding liabilities before applying for conversion.

A common and practical strategy among Indian founders: start as an LLP for the first 2 to 3 years to keep compliance costs low, then convert to a Private Limited Company when you secure your first equity investment or plan to offer ESOPs to senior hires.

14. Winding Up and Closure

LLP: Closure is simpler and cheaper. An LLP can apply for voluntary strike-off by filing Form 24 with the ROC, provided it has no outstanding liabilities or legal proceedings and has filed all pending returns. The process is relatively straightforward for an LLP with clean records.

Private Limited Company: Winding up is more complex. A company can apply for voluntary strike-off under Section 248 of the Companies Act, 2013 by filing Form STK-2 — but requires a special resolution of shareholders, clearance of all liabilities, and filing of pending returns. In cases of disputes or liabilities, formal winding up under the Insolvency and Bankruptcy Code (IBC), 2016 may be required.

LLP vs Private Limited Company — Quick Reference Table

| Parameter | LLP | Private Limited |

|---|---|---|

| Governing Law | LLP Act, 2008 | Companies Act, 2013 |

| Minimum Members | 2 Designated Partners | 2 Directors + 2 Shareholders |

| Tax Rate | 30% + 4% cess (~31.2%) | 25.17% (Section 115BAA) |

| Dividend / Profit Tax | No tax on profit distribution | Dividend taxed in shareholders' hands |

| Statutory Audit | Only if turnover > ₹40L | Mandatory every year |

| Annual Compliance | Lower | Higher |

| Fundraising (VC/Angel) | Not possible | Ideal |

| ESOPs | Not available | Available |

| FDI | Restricted | Broader automatic route |

| Startup India / DPIIT | Eligible | Eligible |

| Closure | Simpler | More complex |

| Ideal For | Professionals, consultants, service firms | Startups, tech companies, scalable businesses |

Which Structure Should You Choose?

Choose an LLP if:

- You are starting a professional services firm — CA practice, law firm, consulting, architecture, or design studio

- You are bootstrapped with no plans to raise equity funding

- You want lower compliance costs and simpler annual filings

- Partners will regularly withdraw profits from the business

- You want the flexibility to manage the business through an LLP Agreement rather than through board meetings and AGMs

- Your initial turnover is expected to be below ₹40 lakhs, keeping you below the mandatory audit threshold

Choose a Private Limited Company if:

- You are building a product, technology platform, SaaS, e-commerce, or any scalable business

- You plan to raise funding from angel investors, venture capitalists, or private equity at any stage

- You want to offer ESOPs to attract and retain key employees

- You are planning international expansion or expect foreign investment (FDI)

- You want to benefit from the lower corporate tax rate under Section 115BAA (25.17% effective)

- Your long-term goal includes an IPO or strategic acquisition

Cost Comparison

Registration costs are generally lower for an LLP than for a Private Limited Company, primarily because there is no stamp duty on share capital and the documentation is simpler.

Ongoing annual compliance costs are also significantly lower for an LLP — particularly for businesses below the ₹40 lakh turnover threshold where no statutory audit is required. A Private Limited Company's mandatory annual audit, board meeting documentation, and ROC filings add meaningful compliance costs every year.

However, as your business grows and requires investor reporting, shareholder agreements, ESOP documentation, and complex ROC filings, the compliance infrastructure of a Private Limited Company becomes a worthwhile investment in governance and credibility.

Frequently Asked Questions (FAQs)

Q1. Can an LLP raise VC funding or angel investment in India?

No. LLPs cannot issue shares or equity instruments — they can only accept partner contributions and loans from third parties. Traditional VC funding, which involves an investor receiving equity shares in exchange for capital, is structurally not possible in an LLP. Venture capitalists and angel investors invest by acquiring equity ownership in a company — and since LLPs have no share capital, there is no mechanism for this.

If an LLP-structured business needs to raise equity funding, it must first convert to a Private Limited Company under the applicable provisions of the LLP Act, 2008 and the Companies Act, 2013. If you are building a startup with any plans to raise external funding at any stage — seed, angel, or Series A — register as a Private Limited Company from day one. Converting later is possible but involves time, cost, and compliance work.

Q2. Which has lower tax — LLP or Private Limited Company?

The answer depends on what you are comparing — the entity-level corporate tax rate, or the effective tax rate on what the owner actually takes home.

At the entity level, a Private Limited Company under Section 115BAA of the Income Tax Act pays an effective tax rate of 25.17% (22% base rate + 10% surcharge + 4% cess) — lower than an LLP's effective rate of approximately 31.2% (30% + 4% cess).

However, when a Private Limited Company distributes profits to its shareholders as dividends, those dividends are taxed again in the shareholders' hands at their applicable income tax slab rate — up to 30% for individuals in the highest bracket. This creates double taxation on the same profit.

An LLP, by contrast, does not tax profit distributions. Partners receive their share of profits tax-free (tax is paid only once at the LLP level at 31.2%). Partners can also receive salary and interest on capital from the LLP, which is deductible for the LLP and taxable as personal income for the partner — often at a lower effective rate.

Practical conclusion: For businesses that plan to reinvest profits and scale (rather than regularly distributing them), a Private Limited Company under Section 115BAA is more tax-efficient at the entity level. For profit-sharing service businesses or professional firms where partners want to withdraw profits regularly, an LLP avoids double taxation and can be more tax-efficient overall. Always consult a Chartered Accountant to model the actual tax outflow for your specific situation before deciding.

Q3. Is compliance really lighter for an LLP compared to a Private Limited Company?

Yes — significantly so, especially for smaller businesses.

An LLP must file only two annual forms with the ROC — Form 11 (annual return, due 30th May) and Form 8 (accounts and solvency, due 30th October) — plus an income tax return. Statutory audit is required only if annual turnover exceeds ₹40 lakhs or capital contribution exceeds ₹25 lakhs. Below these thresholds, accounts can be self-certified by designated partners.

A Private Limited Company must conduct a minimum of four board meetings per year, hold an Annual General Meeting, file Form AOC-4 (financial statements) and Form MGT-7 (annual return), undergo mandatory statutory audit every year regardless of turnover, and file separate forms for every significant corporate event (share allotment, director change, charge creation, etc.).

For a small business or professional practice, this difference in compliance cost and effort is very real — and for many founders, it is the primary reason to choose an LLP in the early years.

Q4. Can an LLP be converted to a Private Limited Company later?

Yes. An LLP can be converted into a Private Limited Company under Section 366 of the Companies Act, 2013 read with the Companies (Authorised to Register) Rules, 2014.

The process requires consent from all designated partners, name reservation on the MCA portal, filing of Form URC-1 with supporting documents (LLP Agreement, certificate of registration, financial statements), and obtaining a fresh Certificate of Incorporation from the Registrar of Companies.

Before applying, the LLP must have filed all pending annual returns (Form 11 and Form 8) and have no outstanding liabilities or legal disputes. The LLP name is generally retained with "LLP" replaced by "Private Limited."

Many founders adopt a two-phase strategy: register as an LLP for the first 2 to 3 years to keep compliance costs low, then convert to a Private Limited Company when they secure their first equity investment or plan to issue ESOPs. This is a legitimate strategy — but conversion involves professional fees, MCA filing costs, and transition time, so it is worth planning carefully with your CA or CS.

Q5. Can an LLP get Startup India (DPIIT) recognition and tax benefits?

Yes. Both LLPs and Private Limited Companies are eligible for DPIIT recognition under the Startup India initiative. Recognised startups can potentially avail a 3-year income tax holiday under Section 80-IAC of the Income Tax Act, exemption from angel tax under Section 56(2)(viib), self-certification under labour and environmental compliance laws, fast-tracked intellectual property applications, and preference in government procurement.

However, eligibility for the Section 80-IAC tax holiday and angel tax exemption is subject to specific conditions — including the date of incorporation, nature of the business (it must be working towards innovation, development, or improvement of products, processes, or services), and turnover limits (not exceeding ₹100 crore in any previous financial year). Not every LLP or Private Limited Company automatically qualifies. A Chartered Accountant should verify eligibility and assist with the DPIIT application.

Q6. What happens if an LLP does not file its annual returns?

All annual filings — Form 11, Form 8, and ITR-5 — are mandatory for every LLP in India, including LLPs that are dormant, have zero transactions, or have not commenced business operations. There is no dormancy window or minimum activity threshold that waives filing obligations under the LLP Act, 2008.

Penalties for late filing are ₹100 per day per form, with no maximum cap — meaning delays of several months can accumulate to significant amounts. An LLP that fails to file for two consecutive financial years risks being struck off the MCA register by the Registrar of Companies. Once struck off, the LLP loses its legal status and restoring it requires a lengthy and expensive legal process.

Additionally, designated partners must complete DIR-3 KYC every year by 30th September. If even one designated partner misses this, their DPIN gets deactivated — blocking all future MCA filings for the LLP until reactivated by paying ₹5,000 per partner.

Q7. Which structure is better for a CA firm, law firm, or consulting practice?

For professional service firms — Chartered Accountants, advocates, architects, management consultants, and similar practices — an LLP is generally the preferred and more practical structure. The key reasons are lower compliance burden and cost, flexible profit-sharing among partners, no double taxation on profit distributions, easier addition or removal of partners as the firm grows, and no mandatory audit unless turnover crosses ₹40 lakhs per year.

A Private Limited Company structure can work for consulting firms too, but the mandatory annual audit, board meetings, AGM, and stricter governance requirements add unnecessary overhead unless the firm is scaling rapidly, raising external capital, or planning to take on institutional clients who require a company structure.

It is worth noting that the Institute of Chartered Accountants of India (ICAI) permits CA firms to practice as LLPs — making the LLP structure particularly well-suited for CA practices.

Q8. Which structure is better if I plan an IPO in the future?

A Private Limited Company, without question. Only companies — not LLPs — can convert into a Public Limited Company and subsequently list on stock exchanges such as NSE or BSE through an Initial Public Offering (IPO) or an SME IPO.

The path to a public listing in India is: Private Limited Company → convert to Public Limited Company → meet SEBI's listing eligibility criteria → file DRHP → IPO.

An LLP has no direct path to a public listing. If an LLP-structured business later decides it wants to pursue an IPO, it must first convert to a Private Limited Company, then to a Public Limited Company — a two-step process that involves significant time, cost, legal restructuring, and potential tax implications.

If an IPO — even a distant one — is part of your long-term vision, register as a Private Limited Company from the start.

Conclusion

Both LLP and Private Limited Company offer limited liability and a separate legal identity — but they are designed for fundamentally different types of businesses and growth paths.

If you are building a growth-oriented startup with plans to raise equity funding, issue ESOPs, scale internationally, or eventually list on a stock exchange, a Private Limited Company is the right structure. If you are running a professional practice, consulting firm, or small service business with no fundraising plans and a preference for simpler compliance and tax-free profit distributions, an LLP offers real advantages in flexibility, cost, and simplicity.

The best structure is the one that matches your actual business goals — not the one that sounds most prestigious or seems most popular. Before registering, always model the tax implications, compliance costs, and funding requirements with a qualified Chartered Accountant.

For expert guidance on business structure selection, LLP registration, Private Limited Company incorporation, DPIIT recognition, startup compliance, and ongoing ROC and tax filings, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from NARESH POKALA & COMPANY. Reach out to discuss your requirements.