PF & ESIC Calculation in India (2026): Complete Guide for Employers

PF & ESIC Calculation in India (2026): Complete Guide for Employers, HR Professionals and Business Owners

Payroll compliance is one of the most critical responsibilities for every business in India. Two of the most important statutory employee benefit schemes — Employees' Provident Fund (EPF/PF) and Employees' State Insurance (ESIC) — directly impact salary processing, employer costs, and employee welfare.

Whether you are a startup, MSME, private company, LLP, factory owner, HR manager, or payroll professional, this guide covers everything you need to know about PF and ESIC applicability, contribution rates, calculation formulas, salary examples, compliance obligations, and important 2026 updates — all in one place.

What is Employees' Provident Fund (EPF)?

The Employees' Provident Fund (EPF) is a mandatory retirement savings scheme administered by the Employees' Provident Fund Organisation (EPFO) under the Employees' Provident Funds and Miscellaneous Provisions Act, 1952.

Under the scheme, both the employer and employee contribute a fixed percentage of wages every month, building a retirement corpus for the employee over time.

Key Benefits of EPF

- Long-term retirement savings

- Pension benefits through the Employee Pension Scheme (EPS)

- Tax benefits under Section 80C of the Income-tax Act, 1961 (subject to applicable limits)

- Partial withdrawals permitted for specified purposes (medical, housing, education, marriage)

- Interest income — EPF interest rate for FY 2025-26 is 8.25% per annum

- Financial security after retirement

EPF Applicability

EPF is generally applicable to:

- Establishments employing 20 or more employees

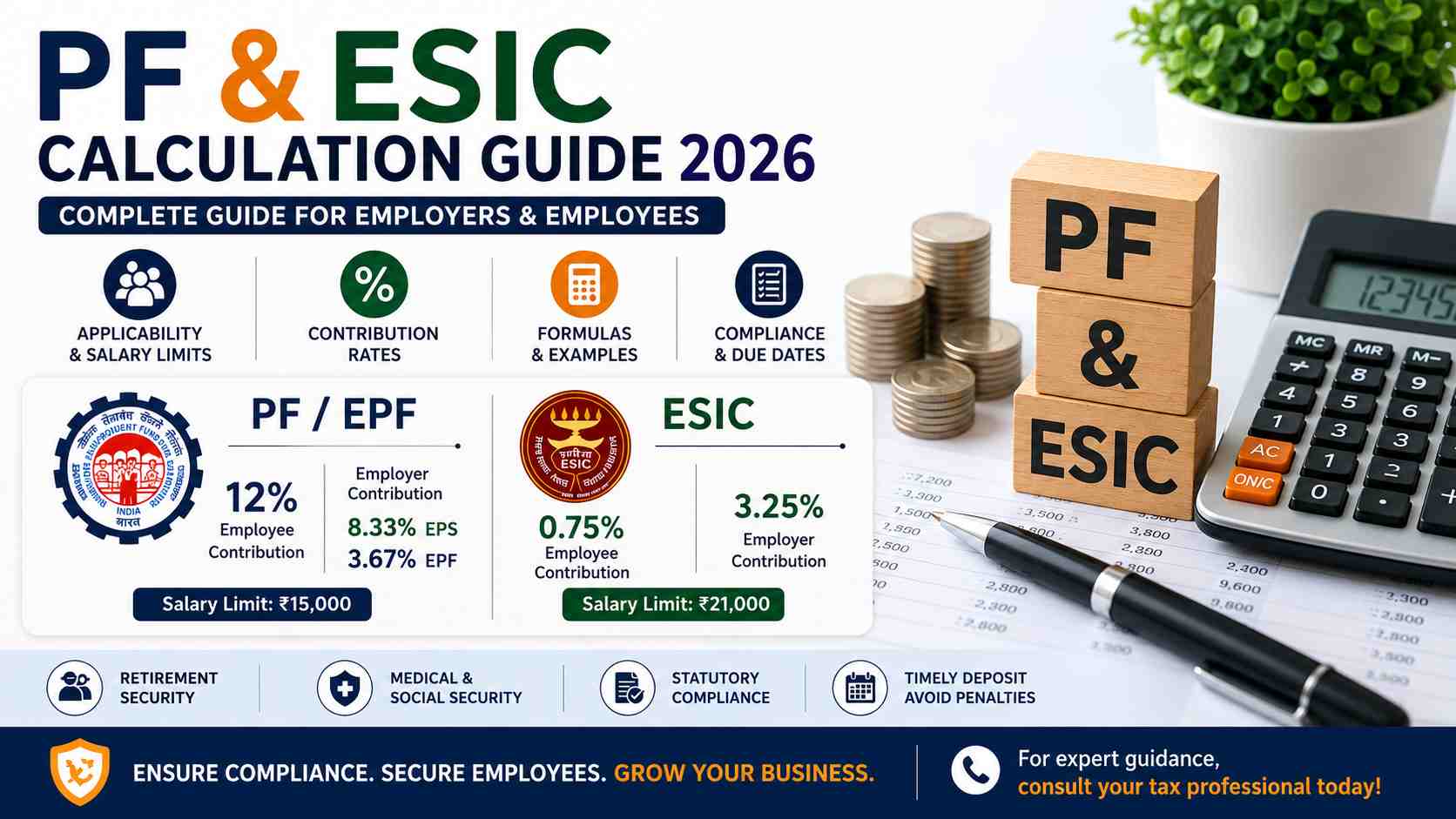

- Employees whose Basic Salary + Dearness Allowance (DA) is up to ₹15,000 per month are mandatorily covered

Important: Once an employee becomes a PF member, coverage generally continues even if their salary subsequently exceeds ₹15,000 per month.

Employers with fewer than 20 employees may register voluntarily, and some industries may have different thresholds under government notifications.

2026 Update — Wage Ceiling Revision Under Review: The Supreme Court of India, in January 2026, directed the Central Government and EPFO to decide on revising the ₹15,000 wage ceiling (unchanged since September 2014) within four months. Employers should monitor official EPFO and Ministry of Labour notifications for any revision that may increase mandatory PF liability.

EPF Contribution Rates

Employee Contribution 12% of Basic Salary + Dearness Allowance (DA)

Employer Contribution 12% of Basic Salary + DA, divided as:

- EPS (Employee Pension Scheme): 8.33%

- EPF account: 3.67%

Additionally, the employer contributes 0.50% towards the Employees' Deposit Linked Insurance (EDLI) scheme and pays administrative charges separately.

Reduced Rate Exception: Employers with fewer than 20 employees, units with sick industry status, or establishments under certain EPFO-notified categories may contribute at a reduced rate of 10%.

PF Calculation Formula

Employee PF = (Basic Salary + DA) × 12% Employer PF = (Basic Salary + DA) × 12%

Practical Example:

Basic Salary = ₹15,000 | DA = Nil

- Employee PF = ₹15,000 × 12% = ₹1,800

- Employer EPS = ₹15,000 × 8.33% = ₹1,249.50

- Employer EPF = ₹15,000 × 3.67% = ₹550.50

- Total Employer PF Contribution = ₹1,800

- Total Combined Monthly PF = ₹3,600

What is the Employee Pension Scheme (EPS)?

EPS is the pension component within the EPF framework, managed by EPFO. Out of the employer's 12% contribution, 8.33% is directed to the EPS account. Employees become eligible for pension benefits upon retirement, subject to a minimum of 10 years of qualifying service.

What is ESIC (Employees' State Insurance)?

The Employees' State Insurance (ESI) scheme is a social security and health insurance programme established under the Employees' State Insurance Act, 1948 and administered by the Employees' State Insurance Corporation (ESIC).

The scheme provides comprehensive medical and financial protection to employees and their families.

Benefits Under ESIC

- Full medical treatment for employees and dependants (from Day 1 of employment)

- Sickness benefit: Cash at 70% of wages for up to 91 days per year

- Maternity benefit: Full wages for 26 weeks (subject to eligibility)

- Temporary and permanent disablement benefits

- Dependants' benefit

- Funeral expenses

- Extended sickness benefit for long-term illness (up to 2 years at 80% wages)

ESIC Applicability

ESIC is applicable to:

- Establishments employing 10 or more employees (20 or more in some states — employers must verify their state-specific notification)

- Employees whose gross monthly wages do not exceed ₹21,000

- For persons with disabilities: the wage ceiling is ₹25,000 per month

Important: ESIC coverage does not stop immediately when an employee's salary crosses ₹21,000. Coverage continues until the end of the current contribution period (April–September or October–March). An employee whose salary exceeds ₹21,000 in, say, January will continue to be covered until 31st March.

ESIC Contribution Rates (Effective since July 2019 — unchanged in 2026)

- Employee Contribution: 0.75% of Gross Salary

- Employer Contribution: 3.25% of Gross Salary

- Total: 4% of Gross Salary

Special provision: For employees earning up to ₹176 per day (daily average wage), the employee's contribution of 0.75% is waived entirely and only the employer contributes.

ESIC Calculation Formula

Employee ESIC = Gross Salary × 0.75% Employer ESIC = Gross Salary × 3.25%

Practical Example:

Gross Salary = ₹20,000

- Employee ESIC = ₹20,000 × 0.75% = ₹150

- Employer ESIC = ₹20,000 × 3.25% = ₹650

- Total ESIC Contribution = ₹800

PF vs ESIC — Key Differences at a Glance

| Particulars | EPF/PF | ESIC |

|---|---|---|

| Governing Law | EPF & MP Act, 1952 | ESI Act, 1948 |

| Authority | EPFO | ESIC |

| Purpose | Retirement Savings + Pension | Medical & Social Security |

| Employee Contribution | 12% of Basic + DA | 0.75% of Gross Wages |

| Employer Contribution | 12% of Basic + DA | 3.25% of Gross Wages |

| Salary Basis | Basic Salary + DA | Gross Wages |

| Wage Ceiling | ₹15,000/month (revision pending) | ₹21,000/month |

| Registration Threshold | 20+ employees | 10+ employees (state-specific) |

How to Calculate Net Salary with PF and ESIC

A standard salary structure consists of Basic Salary, Dearness Allowance (DA), House Rent Allowance (HRA), and other allowances.

Step 1 — Gross Salary = Basic + DA + HRA + Other Allowances Step 2 — Salary Payable (pro-rated for working days) = Gross Salary × (Actual Days Worked ÷ Total Days in Month) Step 3 — Employee PF = (Basic + DA) × 12% Step 4 — Employee ESIC = Gross Salary × 0.75% Step 5 — Net Salary = Salary Payable − Employee PF − Employee ESIC

Example:

Salary Payable = ₹22,100 Employee PF = ₹2,652 Employee ESIC = ₹191 Net Take-Home Salary = ₹22,100 − ₹2,652 − ₹191 = ₹19,257

Employer's Additional Cost — Often Misunderstood

Many employers incorrectly assume that employer PF and ESIC contributions are deducted from the employee's salary. This is not correct.

Employer contributions are an additional cost borne entirely by the employer — on top of the employee's gross salary. They are not deducted from the employee's take-home pay, unless the salary is specifically structured under a Cost-to-Company (CTC) arrangement.

Example of Employer's Total PF & ESIC Cost:

- Employee PF deduction: ₹1,800

- Employer PF contribution: ₹1,800

- Employee ESIC deduction: ₹150

- Employer ESIC contribution: ₹650

- Total Employer Compliance Cost = ₹2,450 (above and beyond the employee's net salary)

Due Date for PF and ESIC Payment

Both PF and ESIC contributions must be deposited on or before the 15th of the following month.

Example: Contributions for the salary month of May must be deposited by 15th June.

Penalties for Late Payment

PF (under the EPF & MP Act, 1952):

- Interest under Section 7Q: 12% per annum on the delayed amount

- Damages under Section 14B: 5% to 25% per annum depending on the length of delay

- Potential prosecution and imprisonment in serious cases of default

ESIC:

- Interest: 12% per annum from the due date

- Damages: up to 25% of arrears for prolonged delays

2026 Key Compliance Updates

- The Code on Wages, 2019 (effective from November 2025) requires the Basic Salary to be at least 50% of total CTC. This effectively increases the PF contribution base for employers who had structured salaries with low basic pay.

- ESIC now extends to gig workers and platform workers under the Social Security Code, 2020 — employers using platform-based workers should monitor their state's notifications for applicable obligations.

- EPF wage ceiling revision is under judicial direction (Supreme Court, January 2026). Employers should prepare for a potential increase in mandatory PF liability.

- ECR 2.0 (EPFO's revamped Electronic Challan cum Return system, launched September 2025) offers improved validation. Ensure your payroll software is compatible.

Common PF and ESIC Compliance Mistakes to Avoid

- Calculating PF on gross salary instead of Basic + DA only

- Calculating ESIC on Basic salary instead of Gross wages

- Not registering with EPFO/ESIC within the prescribed time after crossing the applicability threshold

- Depositing contributions after the 15th deadline

- Incorrect employee classification (part-time, contractual, probationary)

- Errors in ECR filing or UAN mismatches

- Non-maintenance of wage registers and attendance records

- Ignoring new joiners or resigned employees in monthly filings

- Failing to obtain UAN for new employees before first ECR filing

Why Proper PF and ESIC Compliance Matters

Maintaining accurate and timely compliance helps your business:

- Avoid interest, penalties, and damages

- Pass EPFO/ESIC inspections and labour audits without liability

- Maintain accurate payroll and statutory records

- Enhance employee satisfaction, trust, and retention

- Reduce risk of prosecution or legal disputes

- Ensure your employees actually receive the social security benefits they are entitled to

Conclusion

PF and ESIC are among the most important statutory compliance obligations for Indian businesses. Every employer — regardless of size — must understand the applicability conditions, correct wage bases, contribution rates, calculation formulas, due dates, and 2026 regulatory updates.

With the Labour Codes now in force, the EPF wage ceiling revision in progress, and increased scrutiny from EPFO and ESIC authorities, the cost of non-compliance has never been higher. Staying proactive with payroll compliance protects your business and safeguards your employees' long-term welfare.

For expert guidance on PF registration, ESIC registration, payroll processing, ECR filing, labour law compliance, and employee benefit structuring, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from NARESH POKALA & COMPANY. Reach out to discuss your requirements.